How I Saved $1,004 a Year on Insurance in 20 Minutes

Prefer video? Watch the short version on Instagram →

Same coverage. Same deductibles. $1,004 less every year. Here's exactly what I did.

I just saved $1,004 in 20 minutes. Here are the receipts.

I'd been with State Farm for years. Auto and home, both on autopay, both renewing without me ever looking. Last week I finally looked.

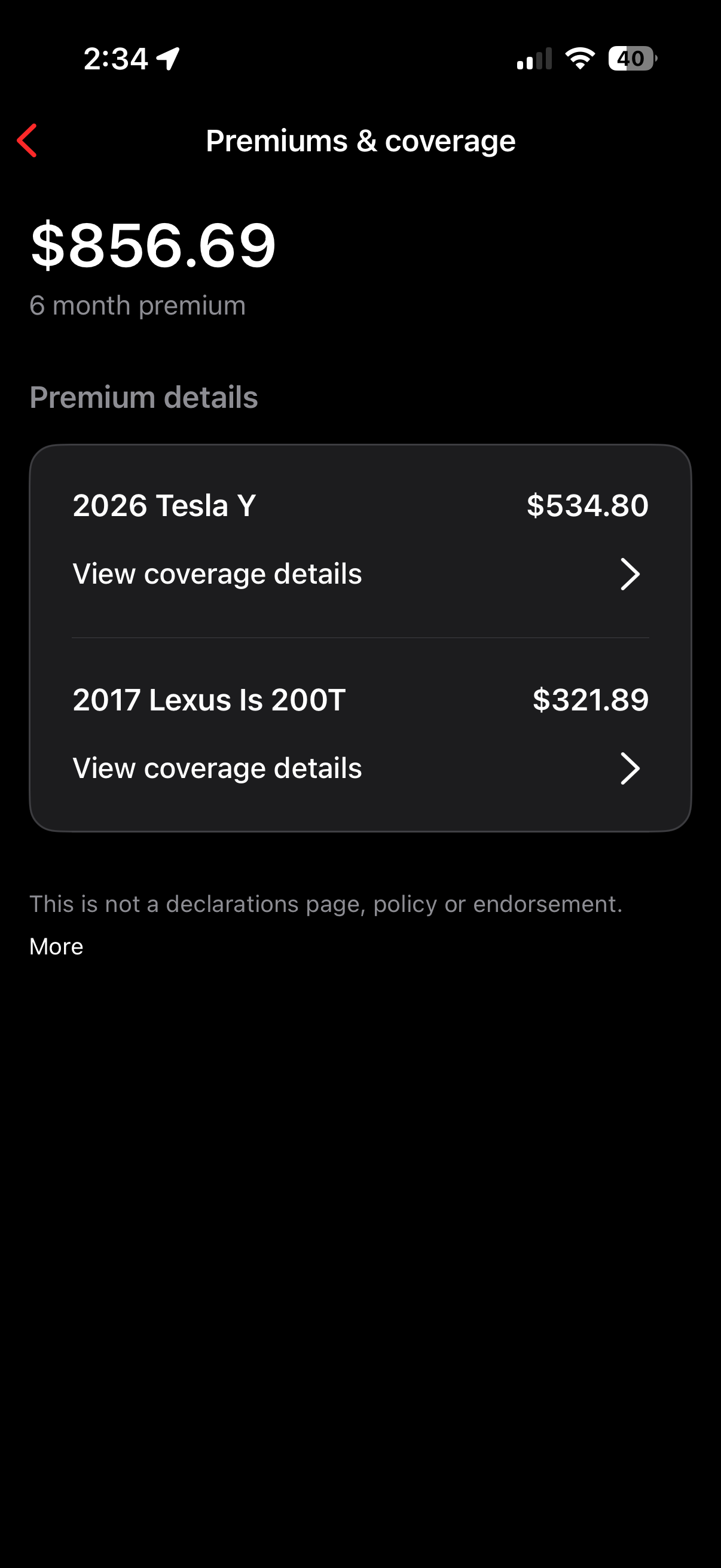

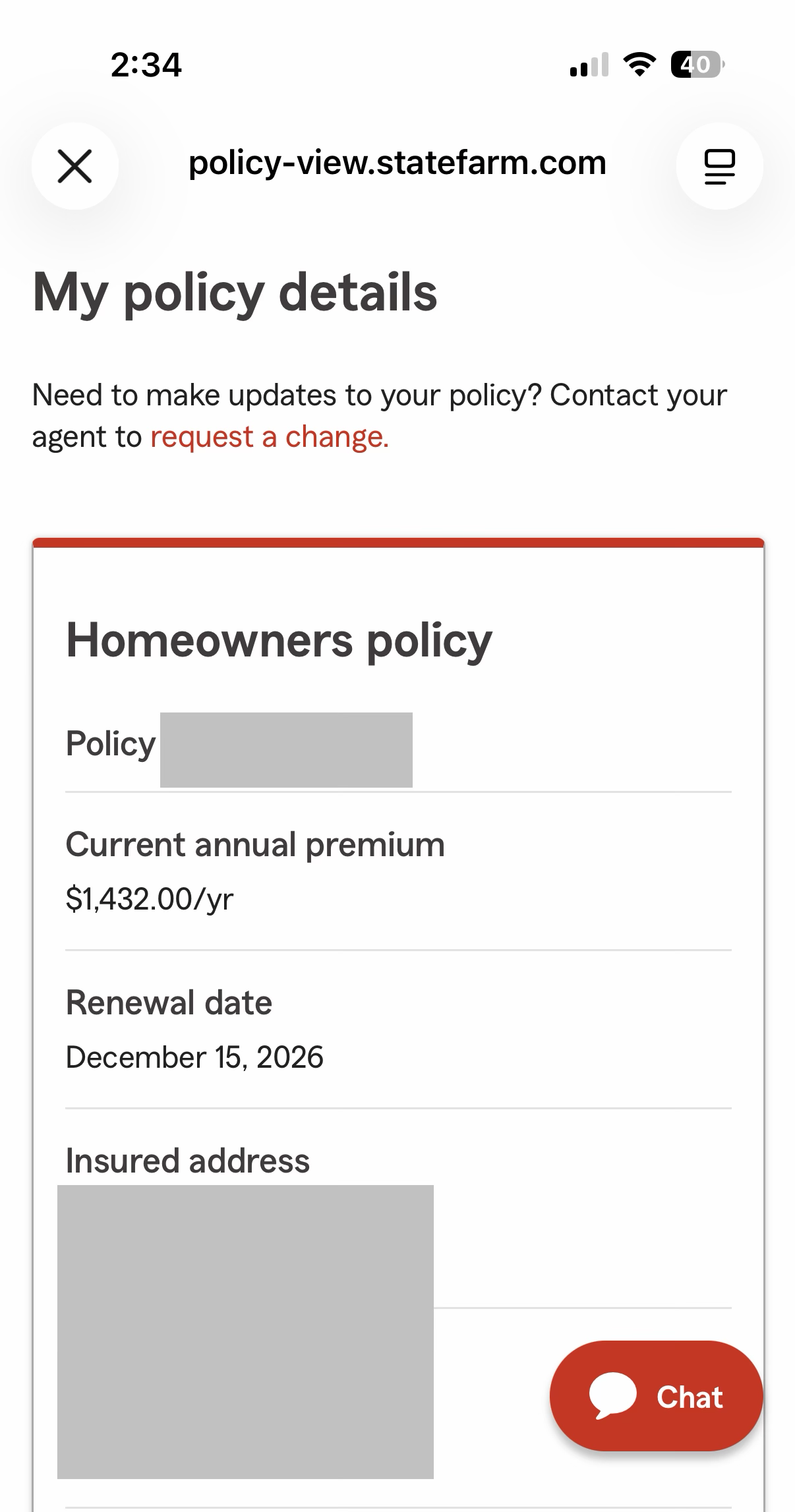

My State Farm auto policy was $856.69 every six months — $534.80 for the 2026 Tesla Model Y and $321.89 for the 2017 Lexus IS 200T. That's $1,713.38 a year. My home policy was $1,432 a year (renews Dec 15, 2026). All in, I was paying roughly $3,100 a year to one company on autopay.

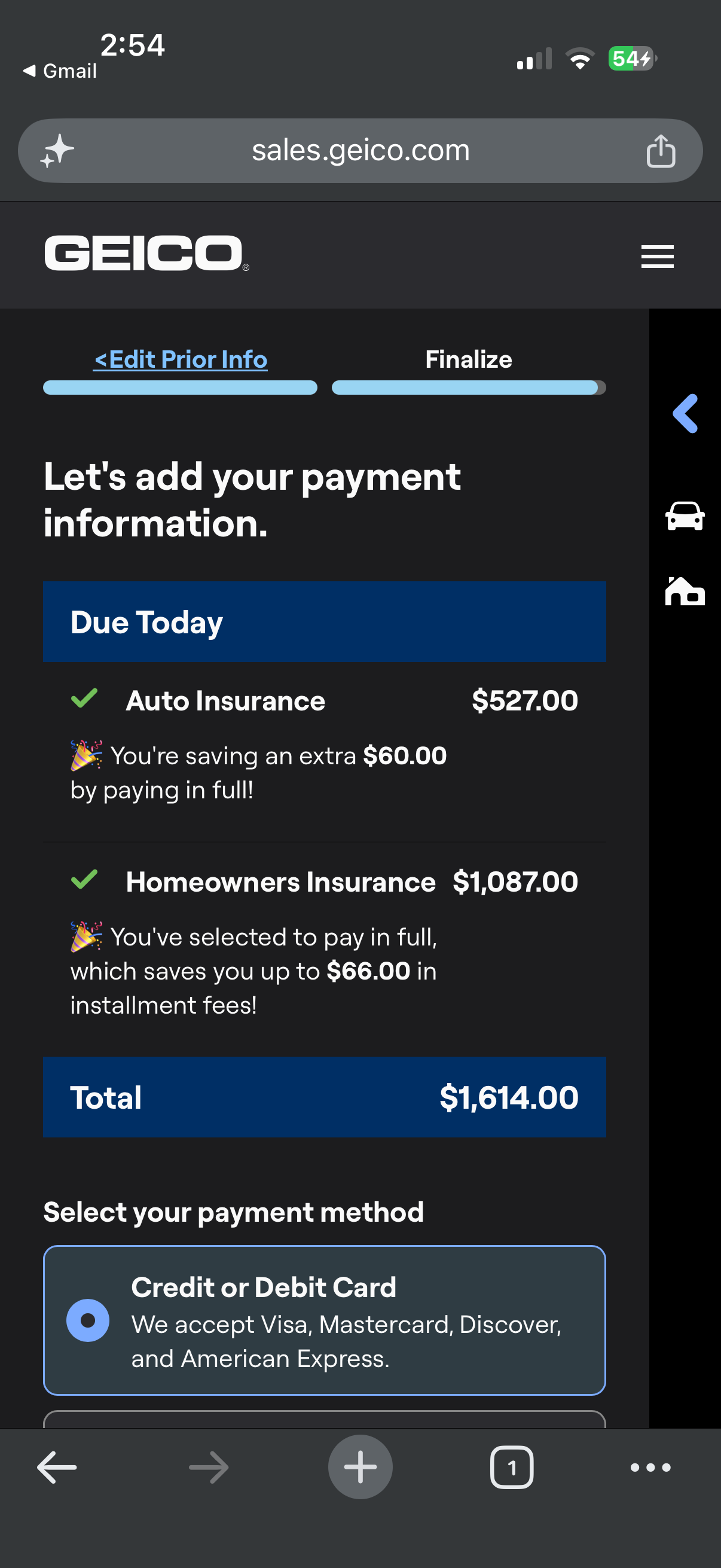

I went to geico.com and ran a quote with the exact same coverage limits and the exact same deductibles. Not a cheaper, thinner policy — a true apples-to-apples match. I bundled auto and home, and I chose to pay in full.

Geico's number: $2,141 a year.

The numbers, side by side

| Policy | State Farm | Geico (bundled) |

|---|---|---|

| Auto (Model Y + Lexus IS) | $1,713.38/yr | $2,141/yr combined |

| Home (renews Dec 15) | $1,432/yr | |

| Total | ~$3,145/yr | $2,141/yr |

| Savings | $1,004/yr — every year going forward | |

Don't take my word for it — here are the actual screens.

Same cars. Same house. Same coverage. Same deductibles. The only thing that changed was the logo on the bill.

This isn't loyalty — it's convenience

Here's the part that actually matters, and it's not about Geico.

Staying with the same insurance company year after year without checking isn't loyalty. It's convenience. And convenience is quietly costing most people $500 to $1,500 a year — every year, forever.

Insurance companies count on this. They give the best rates to new customers and let the loyal ones drift upward at renewal, a little at a time, because they know you won't look. I didn't look for years. That inattention cost me a thousand dollars a year.

The people who build real wealth aren't smarter. They just question every recurring bill: insurance, internet, phone, the subscriptions sitting on autopay that you stopped noticing months ago. None of it is loyalty. It's a tax on not paying attention — and it's the easiest tax in the world to stop paying.

The 4-step playbook

This took me 20 minutes. It'll take you about the same.

- Get a competing quote. Go straight to the big carriers' own sites — Geico, Progressive, State Farm, Allstate. You don't need anything fancy; the carrier sites are free and fast.

- Match your current policy exactly. Same coverage limits, same deductibles as the policy you have right now. This is the only honest comparison — a lower number means nothing if it's a thinner policy.

- Bundle and ask for discounts. Put auto and home together for the multi-policy discount, and ask about paying in full. Geico knocked off about $126 just for paying the year upfront.

- If it's meaningfully lower, switch. Bind the new policy first, then cancel the old one. Never leave yourself with a coverage gap, even for a day.

Honest caveats

I'm not telling you Geico is always the answer. A few things to keep your eyes open about:

- Service and claims can differ. The cheapest premium isn't worth much if the claims experience is a nightmare. Before you switch, check your state's Department of Insurance (DOI) complaint index — it's public, free, and shows you how often people actually complain about a carrier.

- Don't fake the savings. If a quote is lower because the coverage limits dropped or the deductibles jumped, that's not savings — that's just less protection. Match the policy honestly.

- Watch for mid-term fees. Switching before your current policy ends can trigger a short-rate cancellation fee. It's usually small, but ask, so the math still works in your favor.

- Know what's in your quote. Part of my Geico auto price reflects DriveEasy — their optional program that tracks your driving for a discount (about 6% for me). If you'd rather not be tracked, skip it; your number will be a little higher, but the comparison is still worth running.

None of these killed the deal for me. I checked, the numbers held, and I switched.

The close

That $1,004 isn't disappearing — it's just changing destinations. Every year going forward, it's going into my brokerage account instead of Geico's pocket. Invested at the market's long-run average, a thousand dollars a year is real money in a decade.

You won't find a guaranteed return like this anywhere else: 20 minutes of attention, a thousand dollars a year, repeating. The hardest part is just deciding to look.

Comment INSURANCE on the reel and I'll point you to the exact quote setup I used. And follow @joinforbonus for the rest of the Paycheck Playbook — the series where I go through every money move I made to go from zero, one paycheck at a time.

Liked This Post?

Get more like it in your inbox

One short email a week. No spam, no upsells — ever.